What Is Crypto Arbitrage?

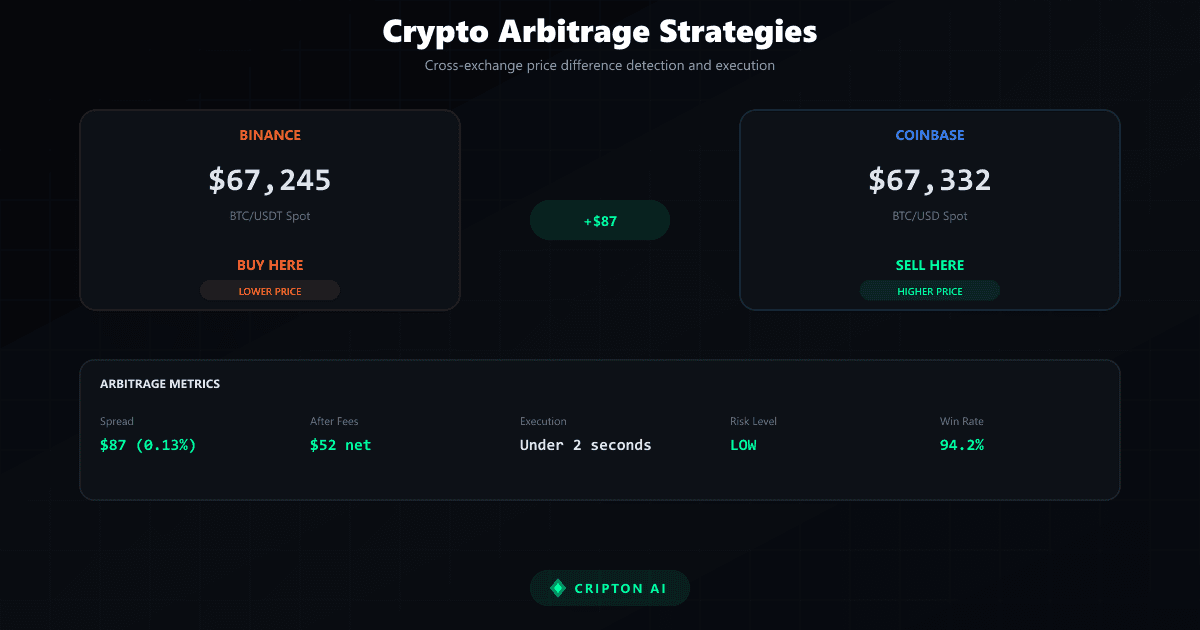

Arbitrage is the practice of simultaneously buying and selling the same asset on different markets to profit from temporary price discrepancies. In cryptocurrency, the same asset (e.g., Bitcoin) may trade at $50,150 on Binance and $49,980 on Coinbase at the same moment, creating a $170 theoretical profit opportunity per BTC traded.

The key word is "theoretical" — execution speed, transaction fees, and transfer times determine whether arbitrage is actually profitable.

Types of Crypto Arbitrage

There are four main arbitrage strategies in crypto: (1) Cross-exchange arbitrage — buy on exchange A, sell on exchange B for a higher price simultaneously. (2) Triangular arbitrage — exploit price differences between three trading pairs on the same exchange (BTC→ETH→USDT→BTC). (3) Statistical arbitrage — use quantitative models to identify historically correlated assets that have temporarily diverged in price.

(4) Funding rate arbitrage — on futures, exploit the difference between spot price and futures price (basis trade).

Why Arbitrage Is Harder Than It Looks

Cryptocurrency markets are increasingly efficient and populated by professional high-frequency trading (HFT) firms with co-located servers and sub-millisecond execution. By the time a retail trader detects a price discrepancy and executes the trade, the opportunity is typically gone. Real arbitrage profitability requires: (1) Co-located servers within exchange datacenters.

(2) Direct market access (DMA) connections. (3) Pre-funded accounts on multiple exchanges simultaneously. (4) Execution latency under 10ms.

Funding Rate Arbitrage: The Accessible Strategy

The most accessible form of arbitrage for retail traders is funding rate arbitrage (basis trading). On perpetual futures contracts (like Binance USDT-M), a funding rate is paid every 8 hours between long and short holders. When the market is bullish, longs pay shorts — if you hold spot BTC and short BTC futures simultaneously, you collect the funding rate while being market-neutral.

This is not risk-free: liquidation risk exists on the futures leg if margin is insufficient during volatile moves.

Transaction Costs vs Arbitrage Profit

The most common reason arbitrage strategies fail to profit: fees exceed the price discrepancy. Example: BTC trades at $50,150 on Exchange A and $50,100 on Exchange B (0.1% spread). If both exchanges charge 0.1% taker fees per leg, your total cost is 0.2% — which exceeds the 0.1% price difference. Profitable arbitrage requires either very low fees (VIP tier), very large price discrepancies (common only during high volatility), or strategies that avoid taker fees entirely.

Risk Warning

Arbitrage is not risk-free. Key risks include: execution risk (the gap closes before your order fills), transfer risk (cross-exchange arbitrage requiring fund movement takes minutes), counterparty risk (one exchange goes offline during the trade), and liquidation risk (futures leg gets liquidated in a volatile move).

Simulated or hypothetical arbitrage results do not account for real execution costs and latency.

Frequently asked questions

What Is Crypto Arbitrage?

Arbitrage is the practice of simultaneously buying and selling the same asset on different markets to profit from temporary price discrepancies. In cryptocurrency, the same asset (e.g., Bitcoin) may trade at $50,150 on Binance and $49,980 on Coinbase at the same moment, creating a $170 theoretical profit opportunity per BTC traded. The key word is "theoretical" — execution speed, transaction fees, and transfer times determine whether arbitrage is actually profitable.

Why Arbitrage Is Harder Than It Looks?

Cryptocurrency markets are increasingly efficient and populated by professional high-frequency trading (HFT) firms with co-located servers and sub-millisecond execution. By the time a retail trader detects a price discrepancy and executes the trade, the opportunity is typically gone. Real arbitrage profitability requires: (1) Co-located servers within exchange datacenters. (2) Direct market access (DMA) connections. (3) Pre-funded accounts on multiple exchanges simultaneously. (4) Execution latency under 10ms.

Sources & references

Cripton AI is not affiliated with these platforms and does not endorse them. Verify each platform’s licensing in your country before using it.

Risk Disclaimer

This guide is for educational purposes only and does not constitute financial, investment, or trading advice. Arbitrage strategies involve execution risks, fee risks, and market risks that can result in losses. Past performance does not guarantee future results. Only trade with capital you can afford to lose.

Ready to start trading?

Create a free account and practice with paper trading — zero risk.

Start Free TrialPrevious Guide

How to Choose a Crypto Exchange: Complete 2026 Guide

Next Guide

Grid Bot Trading Strategy: Complete Guide for Crypto

Keep learning

Live crypto prices

View all prices ›